Supporting Your Aging Parents Without Sacrificing Your Own Stability

It starts gradually. A missed bill here. A forgotten appointment there. Then one day you realize your parents may no longer be able to manage everything on their own. You want to help—but you also have a job, a family, and your own responsibilities. For many adults, stepping in to support aging parents financially or emotionally is one of the most challenging roles they’ll take on.

As life expectancy increases, more Canadians are finding themselves caring for elderly parents while still raising children or building their own future. The emotional weight is one thing—but the financial implications and paperwork can feel overwhelming. The good news? With thoughtful preparation and open communication, you can protect your loved ones while staying grounded yourself.

Start with Honest, Compassionate Conversations

Talking about money, health, or legal documents with your parents isn’t easy. Many people avoid these topics because they’re uncomfortable or feel “too personal.” But waiting until there’s a crisis—like a fall, hospitalization, or memory loss—can limit your options and lead to rushed decisions.

Start with small, respectful conversations. Ask your parents what they would like help with, and offer to support them in ways that don’t feel intrusive. Share a story about someone else who went through this—it can make the conversation feel less like a confrontation and more like a shared concern.

If you have siblings, try to align with them first. It’s helpful to present a united and supportive front, even if only one person is taking the lead. Having an agreed-upon approach can also reduce misunderstandings or resentment down the line.

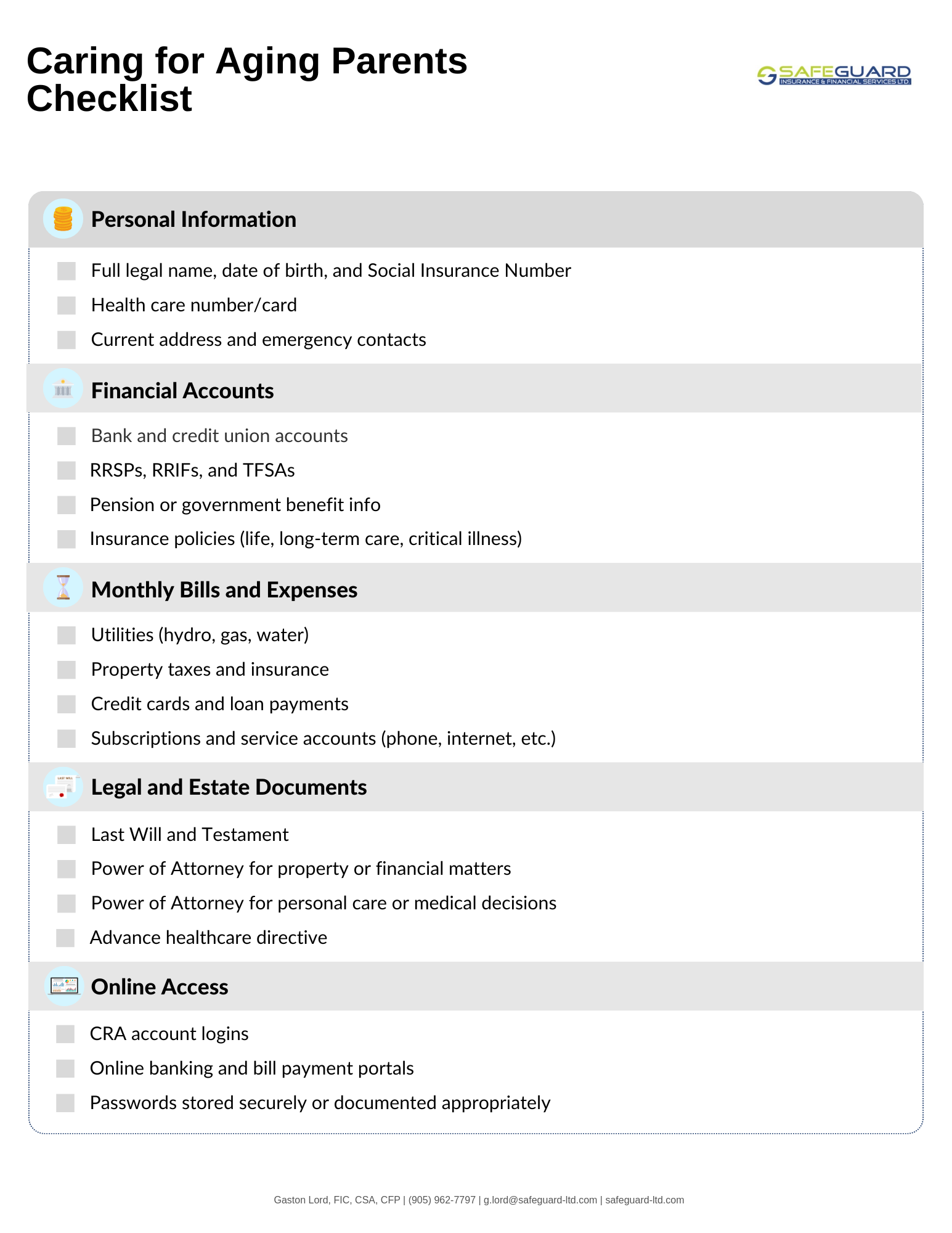

Gather the Right Information Early

One of the best things you can do is help your parents create an “Information Checklist.” This isn’t just about knowing where their money is—it’s about understanding the full picture of their finances, obligations, and preferences.

Here are some items to include in that checklist:

- Personal information: Social Insurance Number, health care card, date of birth, current address, emergency contacts

- Financial accounts: bank accounts, insurance policies, pensions, RRSPs/RRIFs, TFSAs

- List of monthly bills: utilities, credit cards, insurance premiums, phone, internet, property tax

- Legal documents: will, power of attorney (financial and medical), healthcare directive, deeds or titles

- Login credentials (if possible): online banking, CRA account, utility portals

- Health records: medication list, primary doctor, pharmacy, care history

Organize everything into one place—either a binder, secure folder, or encrypted digital file. The goal isn’t to take control right away—it’s to be ready if and when it’s needed

Understand the Legal Side of Helping

Even if your parents trust you to step in, you can’t simply start managing their accounts without legal authority. A power of attorney (POA) document gives you the right to act on their behalf for financial and/or medical matters. This must be signed while your parent is mentally capable.

If you already have POA documents in place, don’t stop there. Reach out to their bank, insurance company, and investment firm to confirm they accept the documents—or if they require their own internal forms. Some institutions may ask for a doctor’s letter confirming incapacity before they will recognize the POA.

Also consider notifying government agencies like Service Canada or provincial health bodies if you have POA status. It can take time for your authority to be processed, so doing it in advance saves delays later.

Without a valid POA, you may need to apply for guardianship or trusteeship through the courts, which can be a lengthy and stressful process.

Create a Plan—And Keep It Flexible

Every parent’s situation is unique. Some may be fiercely independent and want to remain hands-off. Others might be relieved to delegate things like bill payments or appointment scheduling. The key is to agree on a shared plan that respects their wishes while also addressing practical concerns.

For some families, that might mean gradually taking on tasks like organizing bill payments, helping with taxes, or reviewing insurance coverage. For others, it could involve preparing for bigger decisions—like exploring home care options or moving to assisted living.

Try to balance compassion with clarity. It’s okay to say, “I want to make sure everything is in place now, so we don’t have to scramble later.” Helping your parents remain involved in decisions for as long as possible preserves their dignity and autonomy.

You can also revisit the plan as their needs evolve. A yearly check-in to review their financial documents, renew insurance policies, and update contact information is a great habit to adopt.

Use Tools and Resources to Lighten the Load

Managing someone else’s affairs can feel like a second job. Thankfully, there are tools that can help. Automatic bill payments and direct deposit can reduce the risk of missed due dates. Transaction monitoring services can flag suspicious activity and help prevent fraud. Some families use shared calendars or caregiver apps to stay on top of appointments and responsibilities.

Look into local and government resources too. Your province may offer programs that subsidize home care, equipment, or transportation. Some non-profits run adult day programs or offer respite services for caregivers.

If your parents have insurance—like long-term care coverage or disability insurance—review the policy now. Understanding what it does (and doesn’t) cover will help you avoid surprises later.

Moving Forward with Confidence

Caring for aging parents isn’t just about responding to emergencies—it’s about planning ahead so everyone feels supported, respected, and safe. By opening the lines of communication early, organizing important documents, and clarifying legal authority, you’ll be in a much better position to help when it’s needed most.

This stage of life can feel overwhelming, but you don’t have to go through it alone. Start by creating a simple checklist with your parents. Schedule a conversation this month—just one. Taking that small first step today can make a big difference tomorrow. We can help.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or tax advice. Always consult a qualified professional regarding your specific situation. We are not responsible for any actions taken based on this content.